Urgent message: Retail-based healthcare clinics are a growing phenomenon. A report from the California HealthCare Foundation, excerpted here, says public perception is split, and their economic viability remains to be seen. How do their services stack up against those offered by urgent care?

The first in-store clinics appeared in 2000 in the Minneapolis-St. Paul (MN) metropolitan area and were operated by QuickMedx, which later became Minute- Clinic. The company’s founder, Rick Krieger, says the business idea came to him when he tried to get his son in to see a doctor for a strep throat test. He recalls, “We started talking about why there was not a way to just get a simple question answered or a simple test, like strep throat, done. Why was there not some way to just slip in and be seen quickly? Wasn’t there some way to get care in a timely manner for a relatively simple illness? A quick, convenient way to diagnose without waiting in the ER or clinic for two hours? We are not talking about diabetes, cancer or heart disease. We are talking about colds and throat and ear infections.”

1

Krieger and two business partners (one of whom was a family doctor) set up pilot clinics in cooperation with Cub Foods, a local grocery chain. The first clinics charged a $35 flat fee for rapid testing, diagnosis, and prescriptions for 11 common medical conditions, including strep throat, influenza, ear infection, pink eye, and seasonal allergies. They did not accept insurance, which Krieger explains as a deliberate, strategic choice “to compete on a purely retail level and be able to profit on a copayment-type basis.”

The pilot program, though limited, was considered successful, and the founders began to formulate an aggressive growth strategy. In 2005, MinuteClinic appointed a new CEO: Michael Howe, the former CEO of Arby’s. Meanwhile, other clinic companies and retailers entered the game, and there are now a dozen clinic operators running about 90 clinics across the country, a dozen more planning to open clinics in the near future, and hundreds of store openings planned for 2007. As the trend has gathered momentum, the medical and business models have shifted. Most now accept insurance and have expanded their range of services.

Description

In-store clinics measure between 200 and 500 square feet and are quite spare with a simple setup of a reception desk and one or two exam rooms. Retailers often use space that is generating less income per square foot than the clinics are anticipated to provide, so some clinics occupy former video game arcades, vending machine areas, or waiting areas near pharmacies. The retailer has a one-time cost of about $20,000–$100,000 to make the space “broom-ready” (upgrading as deemed necessary by the clinic concept and the contract between retailer and clinic company), and the clinic companies pay for the physical retrofitting. This ranges from $25,000 for a basic clinic with one basic room to $145,000 for a multi-exam room clinic offering broader services; the average setup cost is about $50,000.

Most clinics are staffed with nurse practitioners (NPs) supervised by an off-site physician who is available by phone for consultation, but some clinics employ fulltime physicians. Salaries for NPs are typically much lower than those of physicians. The average salary for an NP in 2005 was $74,812 nationally and $86,674 in California.

3

The clinics use proprietary software systems that claim to provide evidence-based treatment guidelines. These serve as a diagnostic tool as well as a checklist to constrain the types of conditions that can be treated at the clinic. There are referral relationships with local physicians or hospitals for more serious or unusual conditions. Clinics are open extended hours and weekends. Most visits take about 15 minutes and don’t require an appointment. Prices are clearly posted and range from $40 to $70. Some clinics accept insurance and all provide documentation for consumers to file for reimbursement on their own.

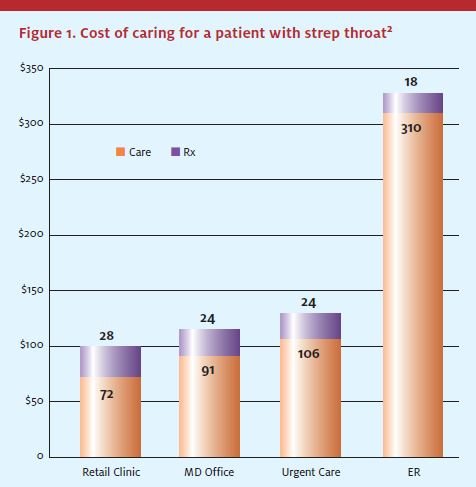

Early usage and cost data, while still quite thin, are beginning to show some patterns. At MinuteClinic, the five most frequently treated conditions are pharyngitis, bronchitis, otitis media, sinusitis, conjunctivitis, and female urinary tract infection. In terms of overhead cost, a preliminary analysis by HealthPartners indicates that on average, MinuteClinic episodes are about 15% less expensive than those initiated at a physician’s office or an urgent care setting, based on one year of claims experience—producing a per-visit savings of $31. (See Figure 1.)

Retail Approach to Healthcare

In many ways, in-store health clinics are a retail experiment that has captured the attention of the healthcare industry. Their existence depends on retail leases, while their success depends on the patronage of customers who may think of their visit as a convenient extension of a shopping trip, and not necessarily an extension of healthcare. Instead of a suite in a medical building or the wing of a hospital, one Florida clinic describes its location as a storefront in a local shopping mall along with “Starbucks, Quiznos, and Planet Smoothie, right next to El Pollo Loco.”4

Retailers are naturally consumer-centric and many of the key players in the retail clinic industry come from consumer backgrounds, such as packaged goods, fast food, and travel companies. It is important to understand how these companies make decisions. Retailers generally see two ways to gain from in-store clinics. On the revenue side, they hope the clinics will attract new customers and drive sales elsewhere in the store, especially prescription and over-the-counter purchases. On the savings side, some retailers see an opportunity to manage the expense of providing healthcare to their employees. Not only are the clinics a relatively cheap way for employers to provide healthcare compared with other care delivery options, but they could reduce absenteeism for doctor’s visits because employees could be treated for minor conditions within the workplace.

However, it is important to note that such scenarios come with a basic caveat: If retailers and clinic companies don’t achieve the expected results, they will close the clinics. Unlike the healthcare industry, retail product life cycles are very short. Retailers continually try new formats and services and are adept at removing less profitable lines of business. In fact, there have already been closings in areas where the clinics didn’t gain sufficient traction. In Baltimore, MinuteClinic is closing its six Target locations after less than two years in operation and opening seven clinics in nearby CVS drugstores. The companies indicated that the closings were not a retreat from the retail clinic concept, but rather a decision to focus on other markets and create different types of service offerings more appropriate to their individual corporate strategies. Either way, this is typical of the retail mentality: fast turnaround, rapid consumer testing, and constant reinvention of the model.

It is also telling that the rollout of in-store clinics has been limited. To put this in perspective, there are more than 3,800 Wal-Mart stores in the United States. Only 14 now have in-store clinics (0.2% of stores) and official plans call for rolling out just 50 more in 2006-2007 (to 1.5% of stores). Of the 100 million people who walk through Wal-Mart’s doors each week, only 1,000 visit a clinic. However, this picture could change. The company has formally stated that it will expand the use of in-store clinics.5 Much will depend on how aggressively Wal-Mart pursues this expansion plan.

Other retailers are approaching these clinics with similar caution, testing them in limited markets and relying on shorter-term contracts with outside clinic companies to evaluate the business impact. This phenomenon could either take off overnight or languish, depending upon whether medical clinics fit into retailers’ overall business strategies and relationships with consumers.

Scope of Practice

Scope of practice varies by clinic company, by state, and by retail location, but there are strategic, practical, and regulatory reasons for in-store clinics to maintain a relatively narrow scope of practice.

Strategically, the clinic model relies on low prices, quick throughput of patients, minimal staff, and proprietary software systems that can reliably manage selective medical diagnoses and information. This is only possible with a short list of simple procedures.

Most in-store clinics are housed in small areas with physical limitations. At most, they have one or two exam rooms with a sink and/or toilet close by (and a few do not even have sinks or private rooms). The clinics explicitly aim to treat common ailments that can be diagnosed quickly and accurately, within 15 minutes. This keeps quality control manageable and overhead low. It also effectively constrains for the range of services they are able to provide for patients. Limited medical records are kept (usually electronically, unless paper backups are required by the state), very little medical equipment is needed, there are no patient gowns (hence no laundry service), and no time-consuming examinations. The diagnostic tests typically offered are compact and rapid and offer simple, accurate results, exempting them from the federal regulations that govern more complex lab procedures.

6

Clinic companies adjust the services they offer inorder to maximize profits and respond to local markets, and there are sometimes differences in scope of practice from one location to the next. To date, most clinics have opened in suburban areas, where affluent shoppers might be willing to pay extra for fast, convenient healthcare. They have emphasized convenience in their marketing, with slogans such as, “You’re sick. We’re quick” (MinuteClinic), “Get well. Stay well…Fast!” (RediClinic), and “Great care. Fast and fair” (Solantic). The clinics initially required consumers to pay in cash for this convenience, but now some insurance companies cover part or all of the in-store clinic visit costs, making the clinics more cost-effective for their subscribers. For these consumers, clinics are at cost parity with a similar visit to a primary care physician, but still have a “time cost” for the consumer to submit the claim.

While the early models focused on “get well” care (diagnosing and treating acute or unexpected illness), the newer model places a greater emphasis on “stay well” care. Web Golinkin, CEO of RediClinic (a subsidiary of InterFit), estimates that his clinics now provide about 75% get-well and 25% stay-well services, with some seasonal fluctuation due to flu shots and school physicials.

7

“We’d like to get to more stay-well,” he says. “We believe that convenience and affordability are just as important to consumers in prevention as they are in treatment, and that consumer interest in preventive services will grow over time.”

In addition, although the clinics started out mainly in suburban enclaves, they are now appearing in less affluent communities where underinsured and uninsured consumers are willing to pay cash for clinic care, not only because it is convenient, but also because they have limited access to healthcare elsewhere.

Regulatory Trends

Regulation of retail clinics varies from state to state. The clinics are typically staffed with NPs who have different degrees of autonomy in each state. In states such as Minnesota (where clinics have the largest presence), NPs can perform a range of functions with no physician on site. In other states, the physician must be physically present for some or all of the time. Each state has different requirements for credentialing and licensing, as well as for physician oversight. These issues may expand, limit—or even prohibit—in-store clinics and the specific services they can provide on a ate-by-state basis. Regulatory requirements for the extent of the physician’s involvement make a significant difference in clinics’ labor costs, so that in some states, although it is technically possible to operate licensed retail clinics, legal practice parameters would make it unprofitable.

Warns RediClinic CEO Golinkin, “If clinics are going to realize their full potential to provide people with easier access to high-quality, routine healthcare at affordable and transparent prices, some of the regulatory barriers in some states will have to be torn down.” Federal support for consumer-driven healthcare makes clinics more attractive by giving consumers incentives to reduce their healthcare spending. In particular, the Medicare Modernization Act of 2003 offers consumers tax incentives for high-deductible insurance plans coupled with healthcare spending accounts to encourage Americans to manage their healthcare expenditures most cost efficiently and mitigate out-of-pocket costs.8

Retail Clinics and the Healthcare Delivery System

Given the many choices consumers have to treat acute episodic ailments, how will the retail clinics compete against or integrate with urgent care clinics, hospital emergency rooms, and primary care physician practices?

Retail-based clinic companies are very careful to distinguish their services from emergency care and primary care providers. They train their staff to refer away any unusual or potentially complicated cases and randomly audit their practitioners on a regular basis to be sure that these standards are being followed.9 When there is some potential overlap of services, the clinics proceed with caution, even if it means foregoing revenues. For example, all three Quick Quality Care locations in Florida Wal-Marts have fully outfitted x-ray rooms with lead-lined walls but are not yet using the equipment because, according to CEO Jack Tawil, “we want to be clear that we’re not an urgent care center.”10

Primary care physicians, whose practices overlap substantially with retail clinics, have been vocal about the downsides of this new site of care. They have expressed concerns about quality and continuity of care, especially in handling patients with serious or chronic conditions. People with chronic conditions are theoretically attractive to retailers and clinic companies—they are otentially very profitable repeat customers—but critics are quick to point out that clinics are not set up to function as a “medical home” for patients with chronic disease.

In response to these concerns, the clinic operators have been firm about their limited scope of practice. For instance, all of them offer treatment for seasonal allergies but most do not treat asthma. Most do not treat chronic conditions such as diabetes. The clinics also form strong referral relationships with doctors in their communities before they open. Sometimes the referral process even works the other way. Michael Howe, CEO of MinuteClinic, says, “In established markets, when physicians understand the model they refer patients to MinuteClinic. For example, on weekends when patients call in, the doctor can say if it’s within the MinuteClinic [scope of practice], so our clinics allow primary care physicians to provide their patients with a better experience…and it frees them up to focus on highrisk or chronic conditions.”

11

In terms of integrating patient information with other providers, all the clinic companies interviewed indicate that they keep centralized electronic medical records that are accessible from any of their locations. These records include a brief medical history taken at the time of service, prescriptions, and test results. If requested, the clinics will print a copy of the record from each visit for the consumer, but they do not electronically transfer the medical records to the primary care physician or referred physician. Each of the clinic companies indicates that they have invested in software to enable the collection and storage of data for patient records in compliance with state and federal regulations. In terms of electronically sharing records, MinuteClinic medical director Woody Woodburn says, “We’re ready to push out data; we’re just waiting for national standards of interoerablility.”9 AtlantiCare plans to integrate its electronic medical record system across its retail clinics, hospitals, urgent care, and primary care locations within 12 to 18 months.

For consumers with insurance, retail clinics can cost more out of pocket than typical copayments for care at other sites. Even clinics that accept insurance usually charge $20 to $25 for a visit (insurers simply discount the standard “menu price” of care by some amount), compared with $10 to $25 copayments for physician office visits and $20 to $100 copayments at the emergency room. Clinics that don’t accept insurance cost much more out of pocket and the charges may or may not be reimbursable if submitted to the insurer. Until this payment disincentive is resolved, clinics will continue to appeal mainly to high-income consumers who are willing to more for convenience, and uninsured consumers who either have no cheaper alternative or cannot afford the wait time or missed work that a visit to a clinic or ER typically entails.

Early Conclusions

Whether retail clinics are a flash in the pan or become a permanent part of the healthcare landscape, their emergence and the reaction of consumers and providers to them raises a series of interesting issues.

As the cost of healthcare continues to rise, employers and governments will continue to shift some of that burden onto employees and will structure incentives for them to seek cheaper care. In the past few years, employers offered reduced copayments for generic prescriptions along with significantly higher copayments for brand name drugs, and consumers responded by opting for generics more frequently. Insurers have already begun to offer a similar financial incentive to use a retail clinic versus the more expensive family doctor, urgent care, or emergency room options. Given the rising number of employers offering high-deductible health plans, this paradigm of consumer financial incentives and disincentives has already started to change the way Americans select and receive healthcare.

The American Academy of Family Physicians, American Academy of Nurse Practitioners, and American Medical Association have all gone on record with opinions about retail clinics. Physician groups urge close physician oversight of non-physician providers working in the retail clinic setting, and nurse practitioners point to the needs of uninsured and under-insured Americans and the potential of retail clinics to offer access. As the clinics become more widespread and more patients and providers have experiences with them—positive and negative—will providers embrace retail clinics as a cost-effective, appropriate adjunct to a primary care provider? Or will physicians and others in the industry reject the clinics?

Retail clinics are a market phenomenon—people elect to use them and generally pay out of pocket. As more Americans use the clinics, we can expect them to “vote with their feet.” People are frustrated with the current system, and most surveyed to date are open to trying clinics but worried that they might be misdiagnosed.12

References

1. “QuickMedx, Inc.” Harvard Business Case 603-049.

2. From confidential report on Blues and MinuteClinic; HealthPartners, 2005.

3. National Salary Survey of Nurse Practitioners. http://nurse-practitioners.advanceweb.com/common/editorial/editorial.aspx?CC=65201.

4. Solantic corporate website: www.solantic.com.

5. “Wal-Mart to expand Employee Health Insurance Plan and In-Store Clinic Use,” New YorkTimes, February 24, 2006.

6. Congress passed Clinical Laboratory Improvement Amendments (CLIA) in 1988 to establish quality standards for laboratory testing and in 1992 published guidelines for waived tests: simple laboratory examinations and procedures that are cleared by the Food and Drug Administration for home use; employ methodologies that are so simple and accurate as to render the likelihood of erroneous results negligible; or pose no reasonable risk of harm to the patient if the test is performed incorrectly.

7. Interview with Web Golinkin, CEO of RediClinic, March 24, 2006.

8. The Wall Street Journal Online. Transcript of Bush Interview, 1/26/2006.

9. Interview with Woody Woodburn, chief medical officer of MinuteClinic, June 4, 2006.

10. Interview with Jack Tawil, chairman and CEO of Quick Quality Care, June 8, 2006.

11. Interview with Michael Howe, CEO of Minute Clinic, April 22, 2006.

12. Harris Interactive poll for The Wall Street Journal, 2005. Available at http://www.harrisinteractive.com/news/newsletters/wsjhealthnews/WSJOnline_HI_Health-CarePoll2005vol14_iss21.pdf.