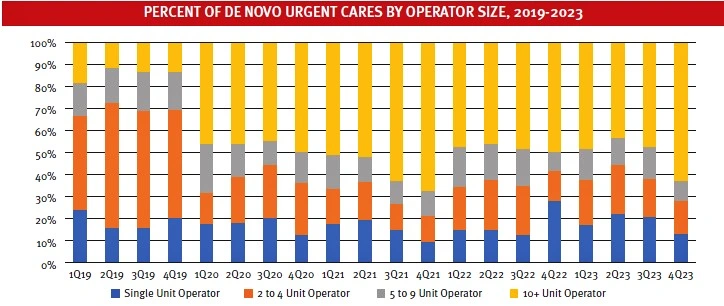

In 2023, the urgent care industry added 1,057 de novo locations—new sites that did not previously exist. But these new centers are far more likely to be owned by larger entities with 10 or more units, also called “enterprise” operators.

In fact, according to data from National Urgent Care Realty analyzed by Experity, for the past 4 years, 10+ unit operators have been the drivers of new rooftop growth. Prior to 2020, the industry was led by the lower midmarket, which consists of the 2-to-4 unit operators. The transition of industry growth dominated by midmarket frontrunners to enterprise frontrunners did not occur over time, but rather represented a sudden, one-time shift early in the pandemic.

Because single-unit operator growth has remained constant, an assumption can be made that enterprise growth most likely came at the expense of midmarket expansion.

Reasons for this shift from midmarket to enterprise growth

acceleration include:

- Some midmarket providers have grown organically to >10 centers and are thus re-classed as enterprise.

- Some midmarket providers were purchased by and folded into enterprise platforms.

- Midmarket providers have attained a level of organizational complexity without the same level of expertise and support in functions like human resources and operations as enterprise companies.

- As a result, midmarket providers have struggled more with post-COVID issues of wage inflation, staffing shortages, turnover, and delayed reimbursement.

- Some midmarket providers are also focused on increasing profitability over growth as they’d like to eventually sell their practice.

Regardless, this indicates a strong trend towards the “corporatization” of urgent care.

Source: National Urgent Care Realty website with Experity analysis. https://www.nationalucr.com/our-database/. Accessed January 19, 2024.

Click Here to download the article PDF