Urgent message: The challenge of running a successful business can be daunting for any entrepreneur. It’s especially tough when your first priority is maintaining excellence as a clinician. The right approach to financial issues can help your business run smoothly—and profitably—while allowing you to focus on caring for patients.

Ask an urgent care physician-owner what the biggest financial obstacle he or she faces is and the answer is likely to be “declining reimbursements.” But what if you found out there is an even bigger challenge to your financial survival—one that is simultaneously global and internal, and one that may be going unnoticed because it’s right under our collective noses?

The fact is that this challenge is the very essence of running an urgent care practice: Physician-owners must look at urgent care not only as a clinical practice, but also as a business entity that has the possibility of real loss when neglected and well-deserved profits if managed consistently and carefully. Physicians need to focus on the practice of being an entrepreneur as well as a care provider. And the reality is that there are times when the physician-owner must focus more on the practice of business management in urgent care.

This does not mean devoting less time to your primary mission; there are several ways that physician-owners can be directly involved in the business of urgent care without sacrificing patient care. A constant and gentle balance can be achieved by adopting a few simple practices that will be explained in this article:

- Routinely reviewing flash reports (customized reports that allow you to see the financial health of your business in areas that interest you, packaged as a timely, redundant flow of information)

- Monitoring the payments at the time of service

- (PATOS) or copays

- Understanding and managing the roller coaster known as cash flow

- Developing and executing a business marketing plan and business plan

- “Negotiating smart” on lease and loan terms

Keep Your Finger on the Pulse of the Business

Good information will yield good decision-making for your business. I recommend that any business operating for less than six months review flash reports daily; all other businesses should review them weekly.

Key financial indicators in urgent care are comprised of some very basic metrics, as well as more complex ones. At minimum, urgent care owners should be focusing on the following metrics to

help build their customized flash report:

Daily Metrics

Patient count – Measures the number of patients who are treated on a daily basis.

Charges – Measures the daily charge volume for all patients seen for a given day.

PATOS – Measures the actual revenue collected from patients at time of service (i.e., copays, generic Rx, ancillary services paid in cash, durable medical equipment, etc.).

Collections – Measures the amount of revenue collected from all other sources (i.e., insurance companies, patient responsibility, occupational medicine revenue from industrial clients, etc.).

Accounts receivable aging – Measures the total revenue that is due your business, broken down into “buckets” (or time).

Weekly Metrics

Procedure count – This can measure the number of specific procedures that are done on a daily or weekly basis.

Checks written – This metric will keep you informed about any money leaving your business.

Other important metrics to monitor are payroll reports, variable expenses, relative value units, personnel costs and benefits, company credit card spending, miscellaneous expenses, employee overtime, and office and medical supply costs. (A relative value unit, or RVU, is a numerical system for describing the value of a medical procedure for the purpose of assigning a price or a charge.

The term “relative value” stems from the idea that each service’s unit value could be measured in relation to the value of other services. A practice can derive its fees by multiplying the unit values by a dollar conversion factor to arrive at a fee or allowable payment.) price or a charge. The term “relative value” stems from the idea that each service’s unit value could be measured in relation to the value of other services. A practice can derive its fees by multiplying the unit values by a dollar conversion factor to arrive at a fee or allowable payment.)

Know Every Dollar Collected at Time of Service

Collecting every dollar that you can at time of service helps to expedite cash flow efficiency, in some cases, by 60 days. Additionally, a patient’s copay amount often represents 25% to 40% of the total collected revenue for that visit.

This practice also helps to increase your personnel’s productivity while reducing the burden on the collection staff. Effective collection of copays at the time of service forces your patient to be part of the utilization management.

After all, do you want the bill you sent to your patient to compete with the credit card bill or phone bill? Chances are your bill is one of the last to be paid.

In addition, if the patient does not frequent your facility or if there are other urgent care facilities in your market, the patient may be inclined to go to your competition because they have not settled the bill with your office.

Effective collection of copays takes time and effort. There can be significant hurdles in determining a copay for a patient’s insurance. Insurance companies do not make it easy to verify coverage or copay amounts.There are subscriptions from third-party vendors that you can buy to simplify verifying insurance eligibility and to make it easier for your medical staff to collect copays.

Another hurdle to overcome is largely internal. Some practices I have worked with have had staff that refused to collect copays because (in their view) “asking for money is bad customer service” or because they are “uncomfortable asking for money before the patient is seen.”

This issue is one of culture. Employee concerns can be overcome with training, constant reinforcement, goal setting, education, and in some cases, reorganization. A staff’s positive attitude is paramount to patient service and will set the tone for the whole office visit. Some offices will not treat patients unless they have paid their copay and settled the balance from past visits.

Others will bill patients the copay amount plus a penalty fee for not paying (usually to cover the cost of the bill sent to the patient). Still others do not collect any copays at time of service and bill the patient after the visit.

These decisions are dependent on how you want to operate your business. However, do not be confused about doing what’s right for your business and what you or your employees perceive to be good customer service.

Executing a strict copay policy takes time and commitment. Set realistic goals (e.g., collect 75% of all potential copays daily the first month this procedure is instituted and work up to a 95% collection rate) and use signs, brochures, and other reminders to help reinforce the policy. Over time, patients will just come to simply expect this as part of the process and you will see a dramatic effect to your accounts receivable balance, as well as a decreased burden on your collection staff.

Understanding the Cash-Flow Roller Coaster

Often, the need for interim, short-term funding comes as a surprise to urgent care owners. Depending on the services provided, most urgent care facilities will experience seasonal ebbs and flows in their business. The billing staff is challenged on an ongoing basis with denials and rejections, forcing accounts receivable farther out on the horizon. Payroll seems to always tighten the purse strings in any business. Quarterly payments for medical malpractice premiums, employee bonuses, and other large expenses can temporarily paralyze an organization.

Understanding cash flow as it pertains to your business is necessary in order to operate on a daily basis, as well as to plan for expansion and growth. If your company does not have access to short-term financing (for example, a business line of credit), you should reconsider if you will be able to weather a financial hiccup in your business. You can usually obtain a small line of credit (under $100,000) based on your personal credit and signature if you are a single owner/practitioner.

For larger organizations, you can usually borrow up to 85% of the total accounts receivable balance. Offering a wider array of services in addition to episodic sick care can also help you maintain a consistent cash flow in the business. If your facility is in a light to heavy industrial area, occupational medicine services such as drug testing (alcohol and blood), breath alcohol testing, employee physicals, hearing tests, and worker injury care can dramatically even out cash flow, as some of these tests can be scheduled in the months during which patient volume typically tapers off.

In order to get a strong hold on cash flow, I recommend that you engage your accounting team in the process. Have regular meetings with your accountant or chief financial officer. Ask them to help you understand what your financial needs are in the short and long term. Challenge them to help you make your business run more smoothly.

In addition, good billing and collection practices, collecting copays at the time of service, and offering pay-for-performance bonuses can help to smooth out cash-flow needs.

Go Through the Motions

Writing a business plan can be one of the most difficult and daunting tasks for any physician owner, CEO, or CFO. However, it is a necessary process in starting, managing, and growing your business.

Ninety percent of my clients (who were already operating before we engaged in a contract) started their business, be it a single-provider practice or a hospital based urgent care clinic, without the existence of a business plan. This, in my opinion, is one of the biggest and most crucial mistakes that you can make (the second one being not keeping your business plan up to date with your company’s current goals).

You need to think of your business plan as your roadmap for success. When done effectively, you will have a written plan that explains what your business is, where it came from (if already in existence), and where you want to take it. By adding past and projected financials, you have documented data that you can use to make crucial decisions as well as share with prospective investors, partners, or bankers.

If you are not comfortable writing a business plan on your own, there are many resources to assist you. Often, your accountant can help you with parts of the plan; however, some may not want to advise you on certain parts of the financial plan so as not to make any false representations as to future earnings.

You may also get off to a good start by buying business plan software; however, many bankers and investors will know a “canned” business plan when they see one, as the finished product may lack originality and look as though not much thought went into it.

Think of your potential audience and decide from there. You may want to contract with a firm specializing in business plan generation. Keep in mind that it is more important to seek the help of someone who knows the industry of urgent care than it is to understand the process of writing a business plan. When analyzing a business plan, content and realistic expectations are more important than the overall visual presentation of the general components to call it a business plan.

From Pain to Progress

Most often, change is inspired by some degree of “pain.” Pain could manifest itself in many forms: decreased reimbursements, higher malpractice premiums, staffing problems, unwelcome competition, or even lack of capacity for business growth.

A good friend taught me a valuable lesson. He once told me, “Change happens when the pain of change is less than the pain of doing nothing.” What he meant is that most businesses will be pushed to make a change when the prospect of changing seems less harmful than if they did not change at all. A business plan will help to prioritize and compartmentalize your businesses goals, strengths, and shortcomings and ultimately guide you through the “pain” of everyday business and make change easier to understand and execute.

“Negotiate Smart” on Leases and Loans

If you speak with any respectable real estate investor, he will tell you that the profit in a deal is made at the time of the purchase, not the sale. That is, you can control many more variables at the time of the purchase than when actually marketing and selling the real estate.

This is often true when obtaining financing via a lease or a loan. Smart negotiation and understanding the factors that can affect a business’s overall risk and exposure will ultimately reduce the risk of loss.

When there is a need for business financing, either via a business loan or a lease, negotiating smart up front can save time and money and reduce business risk and uncertainty. Many companies selling medical equipment can make it very easy to obtain a lease. Often, they require only a personal signature and a quick credit check for the owners and the business, and no historical financial information is necessary. In addition, you can finance 100% of the cost of the equipment, which means that there is no money out of pocket, except for the leasing fees.

However, as easy as a lease can be to obtain, leasing may not be the wisest choice for your business. You will first need to decide which type of financing option is most suitable for each acquisition. I will first say that you should always consult your accountant early in the process. Discuss different scenarios (lease vs. buy) and how each will affect the business’s tax position and its owners as it pertains to their personal tax situation.

Focus on the overall tax advantages or consequences, and how cash flow will be affected. Following are a few tips for financing via a traditional bank loan and lease:

Financing with a traditional bank loan

When today’s office or medical equipment is likely to meet long-term needs (say, seven years or more), purchasing is often the most cost-effective acquisition choice. When looking at a bank loan proposal for such a purchase, focus on the term, rate, collateral required, bank fees, and prepayment penalties.

Make sure the term of the loan matches the useful life of the asset that you are purchasing. You do not want to continue to pay a monthly loan payment on a piece of equipment that is obsolete. In addition, the rate of the loan needs to be competitive. You can verify this by obtaining other proposals from other lenders.

Pay attention to whether you are required to personally guarantee the loan or if the equipment itself is enough collateral to satisfy the requirements of the deal. In any case, shoot for not signing a personal guarantee; however, offering one can be a very powerful and useful bargaining tool.

Banks count on fees for a large part of their profit, so do not be surprised if you are asked to pay a fee to finance the deal. Fees are often quoted in terms of “points.” That is, one “point” is equal to 1% of the total amount financed. Points are very common when financing real estate or a larger piece of equipment. Points are often negotiable and can be waived based on your company’s business relationship with the bank or in the midst of a competing bid from another bank. On a larger financing deal, try not to pay for more than one point. For example, if you are financing a new medical office building at a cost of $1 million, a one-point fee will cost you $10,000.

Last, obtain a loan that does not have a pre-payment penalty provision. This can be very costly for you but can usually be stricken from the loan very easily.

Obtaining a Lease

If your needs are likely to change within the next few years, leasing may be the smarter alternative.

Leasing allows you to acquire the equipment you need today and use it cost effectively until it no longer meets your needs, then upgrade without dealing with it being outdated and obsolete.

Leasing can be easier on cash flow and allow you to upgrade equipment more easily. However, there are some simple pitfalls to avoid when leasing equipment. As you would when using traditional financing, make sure the term of the lease matches the expected life of the equipment. You may find yourself wanting to upgrade but still have to pay the lease out through the last payment. Look for leases that have a built-in allowance for periodic upgrades.

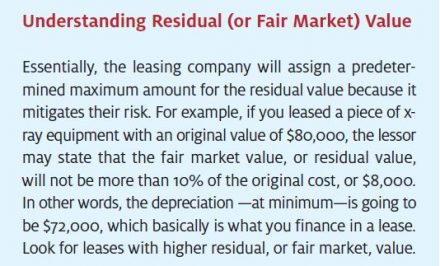

Focus on the residual value—defined as the amount for which a company expects to be able to sell the fixed asset (the piece of equipment) at the end of its useful life—which will ultimately dictate how much that asset has depreciated.

That is, the inverse of the residual value is the depreciated value. In a lease, you do not finance and pay for the total equipment cost; rather, you pay only for the actual amount that you use, or the depreciated value. If you compared two leases with different residual values and all the other factors (term, fees, lease rate factor) were equal, your lease payment would be less with the lease that valued the asset more highly at the end of the lease. (See the box above for a more detailed explanation of residual value.)

Pay attention to the “money factor” when evaluating leases, too. Lease payments are computed by amortizing the depreciation amount over the lease term and applying an interest rate (called the money factor) to the obligation.

Since you will not usually see a stated interest rate in the standard lease contract, it must be computed in order to properly evaluate and compare leasing options. Leasing companies must disclose either the money factor or the interest rate for you.

Most leasing companies will try to confuse you by quoting the money factor as a larger decimal such as 3.04, which really means .00304, because it sounds like a more attractive annual interest rate. Converting this to a standard interest rate in terms more familiar to you can help you avoid excessive interest expense during the term of the lease.

Leasing converters and calculators can be found on the internet and are a good tool in helping you get comfortable with leasing money factors. Or, you can do the conversion yourself simply by multiplying the money factor by 2400 (it is always 2400 and is not related to the length of the loan in months). For example, a money factor of .00304 multiplied by 2400 converts to a corresponding rate of 7.3%.

Last, inquire as to the buyout options on the lease. If you needed to terminate the lease contract early, what are your options? Leases will have a payoff provision equal to the fair market value of the asset at the time of the payoff, or one that is equal to the remaining payments for the life of the lease.

In the latter case, it would not be wise to pay off the lease because you are essentially accelerating 100% of the principle and interest due through the end of the lease.

Conclusion

While focusing on these issues will allow you to be more in tune with the business of urgent care, this is just a starting point at which the physician-entrepreneur can begin to manage and control the business. As in all endeavors, progress takes time to manifest and only continues to move forward with constant, gentle pressure.

In addition, the “pain” that you experience, be it good or bad, will move you to change and allow you to develop your own set of focused initiatives. These initiatives will be a constant reminder and guide you through the perils of business financial management in the urgent care industry.

In the end, with the financial issues in check, you may be able to more effectively focus on what it is that you do best—care for patients who need your expertise as a clinician.