Urgent care in a shifting healthcare delivery environment brings to mind Shel Silverstein’s children’s classic, The Missing Piece Meets the Big O.

In that tale, the missing piece stands alone, waiting for someone to come along and take it somewhere. Various shapes come by, but none are quite right. Some could not roll. Some had too many missing pieces. Finally, a shape comes along that fits just right and they roll along until the missing piece begins to grow and they part ways. Then a full circle, “The Big O,” comes along and the missing piece declares it is what it has been waiting for. The Big O, however, declares it is not missing a piece and that there is nowhere the piece would fit.

Ultimately, the piece learns how to roll alongside the Big O.

Just like that missing piece, urgent care centers have their own navigating to do—through consolidation, narrowing insurance networks, regulatory restrictions, and new payment models like accountable care organizations and medical homes. In the Silverstein story, the piece had to wear off its hard edges so it could roll. Urgent care centers must continuously demonstrate their value to the healthcare system if they are to keep rolling.

The Year Ahead

State regulatory initiatives can offer opportunity for urgent care centers. More often than not, however, they have threatened patient access through policies such as certificate of need or other barriers; these include restrictive licensure or change of control requirements.

While the commercial payers currently dominate the payer mix of urgent care centers, changes to federal programs that favor urgent care open a window for urgent care centers to showcase their value to the non-federal payer community.

TRICARE

In 2016, Congress moved to capitalize on the cost-saving potential of urgent care centers to the TRICARE system—a health insurance program for military service members and their families—and momentum is building for congressional action in 2017 to improve urgent care access for our nation’s veterans. Additionally, the Centers for Medicare and Medicaid Services (CMS) has created a cost-sharing structure within the insurance marketplace standardized plan offerings that encourages urgent care center use over hospital emergency departments.

MACRA

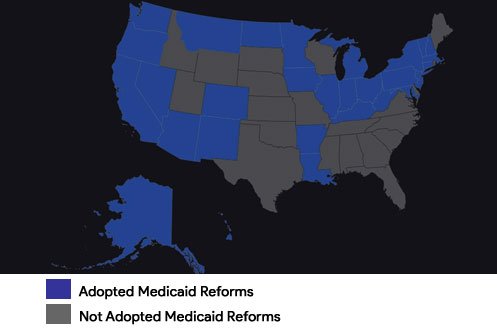

With passage in 2015 of the Medicare Access and CHIP Reauthorization Act (MACRA) and subsequent implementation of the new Medicare physician payment system, or Quality Payment Program, it is expected that states and Congress will turn their attention in 2017 to Medicaid reform. Thirty-two states (including the District of Columbia) have formally expanded Medicaid, while others continue to mull reform options (Figure 1). With a House Republican task force already considering reforms that may be possible in 2017, urgent care centers have an opportunity to position themselves in the reform debate, particularly as newly insured Medicaid patients report difficulty finding a primary care provider and as poor reimbursement to urgent care centers and other providers pushes patients into the emergency department.

Figure 1. The Expanded Medicaid Landscape

ACA

Over the past few years, Republicans have voted nearly 70 times to repeal the Affordable Care Act (ACA). Expect 2017 to constitute the first substantive debate over changes to the law, which could suck much of the oxygen out of healthcare policy discussions.

We also anticipate efforts to address the struggling healthcare exchanges over the next year. With major insurers, including United Healthcare, Humana, and Aetna announcing plans to either scale back or exit the exchanges, countless regions are reeling as they have little to offer those who wish to not only secure insurance through the exchanges, but also avoid the penalties associated with non-participation. United Healthcare’s CEO, Stephen Hemsley, announced that the nation’s largest health insurer would depart many markets in 2017 because of the risks, citing that United could no longer serve these exchanges on an “effective and sustained basis.”1 The gravity of the problem is such that the situation will be untenable in many states unless some reform occurs. There are justifiable concerns of premium price increases in those markets with low to no competition.

Medicare Quality Payment Program

The better bet for healthcare policy watchers is the rollout of the Medicare Quality Payment Program, particularly how quickly Medicare expands alternative payment model (APM) options to physicians and other clinicians and whether APMs are the Medicare program “game changer” they were envisioned to be by policymakers.

Watching what happens with the Quality Payment Program is important for urgent care centers, in part, because some alternative payment arrangements with non-Medicare payers will count toward physicians and other clinicians becoming qualified APM participants under Medicare starting in 2021. This means that an increasing number of physicians will enter into arrangements that put them at financial risk, although with greater upside potential. These providers will be under pressure to control costs while improving patient outcomes. Urgent care centers that are not directly part of these arrangements will need to figure out how to roll alongside, including the provision of solutions to avoidable, costly hospital visits and readmissions.

It may be difficult for urgent care centers that are experiencing growth—or even anticipate growth—in their Medicare patient population to abstain from the new Medicare Quality Payment Program. For most urgent care center providers, the path toward payment will be the Merit-based Incentive Payment System (MIPS). This will calculate payment based on a clinician’s performance in four categories: Quality, Advancing Care Information (or electronic health record use), Cost, and Practice Improvement Activities. The Urgent Care Association (UCA) has stated one of its priorities will be to ensure the program requirements and the metrics for these performance categories are relevant for urgent care providers.

Containing Health Costs

Health expenditures accounted for roughly 32% of the average state’s budget in 2012 and are rising two to three times the Consumer Price Index.2 While Medicare has led payment reform, states trying to “bend the cost curve” will also be looking to create new payment models that may include bundled payments, performance-based reimbursement, accountable care organizations, and cost-sharing strategies, such as those that encourage patients not to use emergency rooms inappropriately. Innovation in more than half of states is being supported and accelerated by a CMS-funded initiative that supports the development and testing of state-led, multipayer healthcare payment and service delivery models.3

One way many health plans are trying to control costs is by contracting selectively with providers, or creating narrow networks. The ACA provides a federal floor of network adequacy protections; however, network transparency and patient difficulty accessing network providers in a timely manner led the National Association of Insurance Commissioners (NAIC) in 2015 to undertake the revision of the network adequacy model law, which states can use as a foundation when considering legislation to regulate network adequacy. UCA lobbied the NAIC to include urgent care as a requirement of network adequacy; while the effort was rebuffed, the revised model law does reflect that a health carrier, as part of its access plan, would need to disclose its method for informing covered persons of the plan’s procedures for covering and approving urgent care to state regulators.

By mid-2016 few state legislatures had introduced or advanced a legislation bill based on the NAIC model.4 If the pace of state network adequacy legislation does not accelerate in 2017, federal regulators, who have deferred to states to date, may be compelled to intervene.

Telemedicine

Having more insured Americans also means further strain on an already overburdened healthcare workforce. An increasing number of states are turning to telemedicine as a cost-effective alternative to face-to-face visits. To expand the reach of providers even further, many states have begun to consider legislation that allows for interstate licensure. In October 2016, eighteen states had passed legislation to join the Interstate Licensure Compact, and others are expected to adopt it in 2017.5 Other telemedicine-policy related issues include coverage and reimbursement, as well as safety and security.

A Big Year Ahead for Urgent Care

Some healthcare delivery systems may find they cannot roll fast enough without integrating urgent care, while others will roll just fine forcing urgent care to adapt. Whichever the case, urgent care centers rely on favorable policies that allow them to prove their value—which is why what happens in federal and state governments this year matters.

Author ID: Camille S. Bonta, MHS is the founder and principal of Summit Health Care Consulting in Breckenridge, CO, focused on the lobbying, regulatory, and advocacy efforts of national healthcare organizations.

References

- La Monica PR. CNN Money: United Healthcare to exit most Obamacare exchanges. April 19, 2016. Available at: http://money.cnn.com/2016/04/19/investing/unitedhealthcare-obamacare-exchanges-aca/.

- Martinez J, King M, Cauchi R, Improving the Health Care System: Seven State Strategies. National Conference of State Legislatures. July 2016 http://www.ncsl.org/Portals/1/Documents/Health/ImprovingHealthSystemsBrief16.pdf

- State Innovation Models Initiative: General Information. https://innovation.cms.gov/initiatives/state-innovations/

- Giovannelli J, Lucia K, Corlette S. Regulation of Health Plan Provider Networks. Narrow networks have changed considerably under the Affordable Care Act, but the trajectory of regulation remains unclear. Health Affairs, July 28, 2016.

- Interstate Medical Licensure Compact. http://www.licenseportability.org